Oil Price Spikes and the Impact on the Economy

23 Mar 2026

Gamma Advisory

Many of us are already feeling the effects of higher fuel prices every time we fill up our cars. This is the most immediate and visible impact for consumers. However, history shows that rising oil prices can have broader and longer lasting consequences for the global economy.

What has happened recently?

Over the past 3 weeks, global markets have been responding to a significant escalation in geopolitical tensions. On 28 February 2026, the United States and Israel launched military strikes against Iran. Initially, markets expected the conflict to be short-lived, given the overwhelming US-Israeli military strength involved and the assumption that Iran would be forced to capitulate quickly.

What markets did not anticipate was Iran’s response. Iran has since closed the Strait of Hormuz and begun using its control of this critical waterway as economic leverage. This is a major development, as the Strait of Hormuz is one of the most strategically important energy corridors in the world.

Iran has openly stated that it is prepared to prolong the conflict and inflict economic damage globally by keeping the strait closed. This escalation has shifted the focus from a short military conflict to a potentially extended economic shock.

Why does the Strait of Hormuz matter?

Oil and energy are at the centre of modern economies, but the impact goes well beyond fuel prices:

- Around one third of the world’s nitrogen fertiliser feedstock moves through the Strait of Hormuz, placing pressure on global food prices.

- More than 90% of the world’s sulphur is produced as a by-product of oil and gas refining. This puts supplies of sulphuric acid at risk.

- Sulphuric acid is arguably one of the world’s most important industrial chemicals, used in mining, manufacturing, agriculture and infrastructure.

- Numerous other supply chains, including polyester, plastics, asphalt and construction materials; are also vulnerable to disruption.

If the conflict continues for several months, these disruptions could significantly affect global growth, inflation and financial markets.

The economic risk: stagflation

Some commentators have likened the current environment to a COVID 2.0supply chain shock. Reduced supply combined with ongoing demand could push prices higher across many goods and services. The more concerning risk is stagflation, a scenario where inflation rises sharply while economic growth slows. In this environment, central banks have limited options. Cutting interest rates may worsen inflation, while raising rates could further weaken growth. That said, it is important not to jump to worse-case conclusions prematurely. History provides some useful perspective.

What does history tell us?

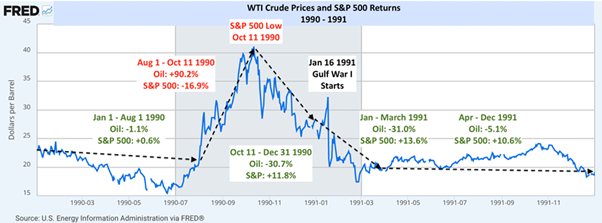

A relevant comparison is the 1990 Gulf War, when Iraq invaded Kuwait on 2 August 1990:

- Crude oil prices rose nearly 90% over the following 2 months

- Over the same period, the S & P 500 fell 16.9%

- From October 1990 to the end of the year, oil prices began to retreat by about 30% and the S&P 500 rebounded by 11.8%.

This occurrence clearly illustrates the inverse relationship between oil prices and global markets. Rising oil prices tend to pressure markets, while falling oil prices often provide relief.

At present, oil prices remain one of the most important drivers of market direction.

The chart below clearly illustrates the relationship between movements in the oil prices and their impact on financial markets.

So, where do markets go from here?

While there is still a great deal of uncertainty (Trump seems to think he can ‘control’ this war), current research suggests there are three potential scenarios that could unfold from here. The key variables remain – the duration of the conflict, and the path of oil prices.

- Conflict ends soon (best-case scenario) – the conflict in Iran concludes within the next month and oil prices retreat from recent highs. While the global economy would experience a short-term shock, conditions would likely stabilise over time. In this scenario, markets may recover from current levels.

- Prolonged conflict with gradual improvement – the conflict continues for several months, keeping oil prices elevated eventually before they gradually ease over the next 12-18 months. This would be a challenging environment, but the global economy may manage to “muddle through”. Markets could remain weaker in the shorter term before improving as conditions stabilise.

- Extended conflict (worst-case scenario) – the conflict continues for the remainder of 2026, with oil prices remaining high due to ongoing supply constraints. In this scenario, markets would fall sharply and the risk of a global recession would be significantly elevated.

While the third scenario is currently less likely than the first two, its probability increases the longer this conflict persists and oil price remains high.

What does this mean for investors?

As investors, it is important to focus on what we can control. We cannot control geopolitical events or oil prices, but we can control how our investment allocation (portfolios) is positioned to manage uncertainty.

We encourage clients to review their current asset allocation to ensure they have:

- Appropriate levels of cash and liquidity, and

- Sufficient exposure to more defensive, income producing assets where suitable.

Please feel free to reach out at any time to discuss your personal circumstances, portfolio positioning and asset allocation in more detail.